TL;DR:

- A lease quote combines depreciation, finance charges, and taxes to form your monthly payment.

- Understanding the calculation helps you verify dealer offers by reviewing key figures like the net capitalized cost, residual value, and money factor.

A lease quote is calculated by combining three core components: the depreciation fee, the finance charge (called the rent charge), and applicable taxes. These three figures together produce your monthly payment. Understanding the lease quote calculation process puts you in a far stronger position when you sit down with a dealer, because you can check every number before you sign.

The standard lease payment formula is: Monthly Payment = Depreciation Fee + Rent Charge + Monthly Tax. Each of those three parts depends on variables you can influence, including the negotiated vehicle price, the money factor, and the lease term. Knowing how leasing rates are determined means you can spot where a dealer is padding the numbers.

How are lease quotes calculated?

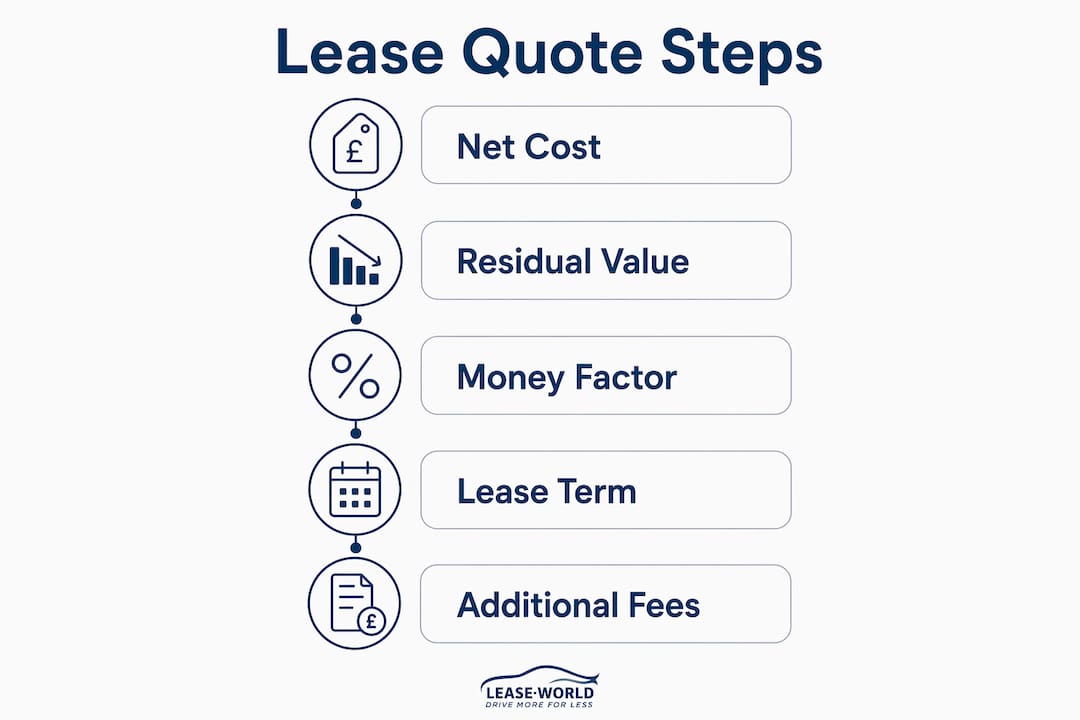

The lease quote calculation process starts with three named figures: the net capitalised cost, the residual value, and the money factor. Get these right and the rest of the maths follows cleanly.

Net capitalised cost is the adjusted price of the vehicle you are financing. The net cap cost formula is: Negotiated Price + Fees minus Cash Down Payment minus Trade-In minus Rebates. A lower net cap cost directly reduces both your depreciation fee and your rent charge.

Residual value is the predicted worth of the car at the end of the lease, expressed as a percentage of the manufacturer's suggested retail price (MSRP). The leasing company sets this figure. A higher residual value means you are financing a smaller slice of the car's total value, so your monthly payment falls.

Money factor is the lease equivalent of an interest rate. It looks like a tiny decimal, such as 0.00200. Multiply any money factor by 2,400 and you get the approximate APR equivalent. A money factor of 0.00250 equals a 6.0% APR. That conversion is the single most useful tool for comparing a lease against a traditional loan.

Once you have those three figures, the two payment components work like this:

- Depreciation fee: (Net Capitalised Cost minus Residual Value) divided by the number of months in the lease term.

- Rent charge: (Net Capitalised Cost plus Residual Value) multiplied by the money factor.

- Monthly tax: Applied to the sum of the depreciation fee and rent charge, at your local rate.

Pro Tip: Negotiate the capitalised cost and money factor before you discuss monthly payments. These are the two levers that actually move the number on your bill.

How do specific factors affect your lease quote?

Several variables feed directly into the lease pricing methodology, and each one shifts your monthly payment in a measurable way.

Negotiated sale price is the most powerful factor. Every pound you reduce the selling price reduces the net capitalised cost by the same amount. That saving flows through both the depreciation fee and the rent charge, so the benefit compounds across the full term.

Lease term affects how the depreciation is spread. A 36-month lease divides the same depreciation over fewer months than a 48-month deal, which raises the monthly figure. Longer terms lower the monthly payment but increase total rent charges paid over time.

Mileage allowance changes the residual value. Higher annual mileage means the car is worth less at the end of the lease, so the residual drops and your depreciation fee rises. Standard mileage allowances typically sit at 10,000–12,000 miles per year. Exceeding that limit triggers excess-use fees that do not appear anywhere in the base payment calculation. You can read more about choosing the right mileage before you commit to a contract.

Fees and down payments both adjust the net capitalised cost. Acquisition fees, administration charges, and dealer fees added to the cap cost increase your monthly payment. A down payment (called a cap cost reduction) lowers it. The key distinction is whether fees are paid upfront or rolled into the cap cost.

- Upfront fees: paid once, no financing cost attached.

- Rolled-in fees: added to the cap cost, so you pay interest on them for the full lease term.

- Down payments: reduce the cap cost but are lost if the car is written off.

- Rebates and trade-in values: reduce cap cost without requiring cash from your pocket.

Pro Tip: Ask the dealer to list every fee separately before they quote a monthly payment. Rolled-in fees are invisible in the headline figure but cost you more over the term.

How to compare lease quotes effectively

Comparing lease quotes accurately requires separating the depreciation portion from the finance portion. Most dealers present a single monthly figure, which makes it impossible to see where the cost is coming from.

Capitalised cost and money factor negotiations are the principal ways to reduce monthly payments. Residual value is fixed by the leasing company and cannot be negotiated. That said, choosing a vehicle with a higher residual value is one of the most effective ways to lower your payment without negotiating at all.

Converting the money factor to APR is the clearest way to compare a lease against a bank loan or personal contract purchase. Multiply the money factor by 2,400 and compare that percentage directly against other finance rates on offer.

| Quote component | What it tells you | Can you negotiate it? |

|---|---|---|

| Net capitalised cost | The effective purchase price you are financing | Yes, negotiate the sale price down |

| Residual value | The car's predicted end-of-term worth | No, set by the leasing company |

| Money factor | The finance rate applied to the lease | Yes, ask for the buy rate |

| Acquisition fee | Admin charge from the leasing company | Sometimes, or ask for it to be waived |

| Dealer markup on money factor | Extra profit hidden in the finance rate | Yes, if you know the base rate |

Dealers often mark up the money factor above the base buy rate, increasing finance charges without any visible change to the headline payment. The only way to catch this is to know the manufacturer's published money factor before you walk in.

Pro Tip: Run your own calculation using the vehicle's MSRP, the published residual percentage, and the manufacturer's money factor before visiting any dealership. If the dealer's quote is higher, you know exactly where to push back.

What are common misconceptions about lease quote calculations?

The monthly payment is not the total cost of the lease. This is the most common and costly misunderstanding in the entire lease quote estimation process.

The total cost includes the initial rental (often three months upfront), all monthly payments, any fees rolled into the cap cost, and potential charges at the end of the term. Rolling fees into the capitalised cost lowers your upfront outlay but raises the financed balance, which means you pay interest on those fees for every month of the lease.

Several other points catch people out:

- Residual values look like percentages but work as pound amounts. A 58% residual on a £30,000 car means the leasing company treats the residual as £17,400 in the calculation. Always convert the percentage to a cash figure to check the maths.

- Sales tax treatment varies. In the UK, VAT is applied to each monthly payment rather than to the full vehicle value upfront. The rate you pay depends on whether the lease is personal or business.

- Excess mileage and wear charges are not in the base quote. These fees only appear at the end of the contract if you exceed limits. They can add hundreds of pounds to the real cost of the lease. Find out more about what happens if you exceed lease mileage so you are not caught out.

- A low monthly payment can hide a high total cost. A longer term or large initial rental can make the monthly figure look attractive while the overall spend is higher than a shorter deal.

How to calculate your own car lease quote

Working through a real example is the fastest way to make the formula stick. The figures below are illustrative, based on typical UK lease structures.

-

Set the vehicle price. Assume a car with an MSRP of £30,000. You negotiate the selling price to £28,500. The dealer adds a £500 acquisition fee. No down payment is made. Net capitalised cost = £28,500 + £500 = £29,000.

-

Calculate the residual value. The leasing company sets the residual at 50% of MSRP over 36 months. Residual value = £30,000 × 0.50 = £15,000.

-

Calculate the depreciation fee. (Net Cap Cost minus Residual Value) divided by term = (£29,000 minus £15,000) divided by 36 = £14,000 divided by 36 = £388.89 per month.

-

Calculate the rent charge. (Net Cap Cost plus Residual Value) multiplied by money factor = (£29,000 plus £15,000) multiplied by 0.00200 = £44,000 multiplied by 0.00200 = £88.00 per month.

-

Add the pre-tax payment. £388.89 + £88.00 = £476.89 per month before tax.

-

Apply VAT. At 20% on the full monthly payment: £476.89 multiplied by 1.20 = £572.27 per month.

A stepwise calculation like this lets you verify every line of a dealer's quote. If their figure is higher, the gap is almost always in the capitalised cost or the money factor.

Pro Tip: Take your completed calculation to the dealership. Showing a dealer you have done the maths changes the entire negotiation dynamic.

Key takeaways

A lease quote is built from three fixed components: depreciation, rent charge, and tax. Knowing each one gives you the tools to assess any offer accurately.

| Point | Details |

|---|---|

| Core formula | Monthly payment equals depreciation fee plus rent charge plus monthly tax. |

| Net capitalised cost | Negotiate the sale price down to reduce both the depreciation and finance portions. |

| Money factor conversion | Multiply the money factor by 2,400 to get the APR equivalent for rate comparisons. |

| Residual value is fixed | The leasing company sets residual value; choose a high-residual car to lower payments. |

| Total cost vs monthly payment | Always calculate the full lease cost including fees, initial rental, and potential end charges. |

What I have learned from watching people negotiate leases

Most people walk into a dealership focused entirely on the monthly payment. That single number is the dealer's greatest advantage. It hides the money factor markup, the rolled-in fees, and the inflated cap cost all at once.

The dealers who mark up the money factor do so because almost nobody checks it. The base buy rate is published by manufacturers, but most consumers never look it up. Spending ten minutes finding that number before you visit a showroom is worth more than an hour of haggling on the day.

The other thing people consistently underestimate is the total cost of ownership across the full term. A £350 per month deal over 48 months with a large initial rental can cost more in total than a £420 per month deal over 36 months with no initial payment. The monthly figure is almost meaningless without the full picture.

My honest advice: build your own calculation before you go anywhere near a dealer. Use the formula in this article, check the manufacturer's published residual and money factor, and walk in knowing what the payment should be. If the dealer's quote is higher, you know exactly which line to question.

— Jason

Get transparent lease quotes with Lease World

Lease World takes the guesswork out of the lease quote calculation process. Every quote is broken down clearly, with no hidden fees and no marked-up money factors buried in the small print.

Whether you are looking for a personal car lease or need guidance on how leasing rates are determined for your specific situation, Lease World's team provides honest, detailed comparisons. Browse the full range of UK leasing guides to go deeper on any part of the process, or request a personalised quote and let the team do the calculation for you. Fixed monthly payments, no deposit options, and free UK delivery on eligible vehicles make it straightforward from the start.

FAQ

What is the basic formula for calculating a lease payment?

The standard lease payment formula combines three parts: the depreciation fee, the rent charge, and monthly sales tax. Each part depends on the net capitalised cost, residual value, money factor, and lease term.

Can I negotiate my lease quote to get a lower monthly payment?

Yes. The two components you can negotiate are the capitalised cost and the money factor. Residual value is set by the leasing company and cannot be changed, but choosing a vehicle with a higher residual naturally reduces your payment.

What does rolling fees into the cap cost actually mean?

Rolling fees into the cap cost means adding charges such as acquisition or administration fees to the financed amount rather than paying them upfront. This increases the total rent charge paid over the lease term because you are effectively paying interest on those fees.

How do I convert a money factor to an interest rate?

Multiply the money factor by 2,400 to get the equivalent APR. A money factor of 0.00200 equals a 4.8% APR. This lets you compare a lease directly against a bank loan or other finance product on equal terms.

Are excess mileage charges included in my monthly lease payment?

No. Excess mileage fees are not part of the base monthly payment calculation. They are charged at the end of the lease if you exceed the agreed annual mileage limit, so they must be factored into your total cost estimate separately.