TL;DR:

- Car leasing (Personal Contract Hire) involves paying for vehicle use over a fixed term rather than ownership.

- Comparing deals requires evaluating total costs, including upfront payments, monthly rentals, mileage, and contract length, not just monthly prices.

Car leasing, formally known as Personal Contract Hire (PCH), is a fixed-term rental agreement where you pay to use a vehicle rather than own it. To compare car lease deals properly, you must evaluate the total contract cost: upfront payment, monthly rentals, mileage allowance, and contract length together. Focusing on the monthly price alone is one of the most common and costly mistakes UK drivers make. Providers like Lease World, Parkers, and Leasing.com all display deals differently, which makes a structured comparison method non-negotiable.

Which costs should you compare in a car lease deal?

The total cash outlay across the full contract is the only number that matters when comparing lease deals. Deals focused on monthly payment alone can mislead because they ignore differing upfront payments and mileage terms. Two deals with identical monthly prices can cost thousands of pounds apart over a three-year term.

Here are the core cost components you must gather for every deal you compare:

- Initial rental (upfront payment): Typically three to twelve monthly rentals paid at the start of the contract. A higher upfront payment reduces your monthly cost but increases your day-one financial exposure.

- Monthly rental: The fixed payment made each month for the duration of the contract.

- Contract length: Usually 24, 36, or 48 months. Longer terms often reduce monthly cost but increase total commitment.

- Mileage allowance: The annual mileage cap written into the contract. Exceeding it triggers per-mile charges.

- Maintenance package: Some deals include servicing, tyres, and breakdown cover. These add monthly cost but reduce surprise bills.

To compare deals on equal terms, use this formula: (initial rental ÷ contract months) + monthly payment = true monthly cost. Spread the upfront payment across the term so you are comparing like for like. A deal with a nine-month initial rental and £199 per month is not cheaper than a deal with a three-month initial rental and £229 per month. You need the maths to confirm it.

Pro Tip: Always check the payment profile options before signing. Choosing a lower initial rental increases monthly cost, but it also reduces the money you lose if the vehicle is written off early in the contract.

The Financial Conduct Authority requires leasing advertisements to display initial rental, term length, and mileage alongside the monthly price. If a deal you are looking at omits any of these, treat it with caution.

How does mileage allowance affect your lease cost?

Mileage allowance is the single most underestimated financial variable in a car lease deal. Excess mileage charges typically range between 3p and 15p per mile, and those pennies accumulate fast. A 2,000-mile annual excess on a three-year lease can easily cost £360–£900 at return, depending on the rate written into your contract.

The right approach is to estimate your realistic annual mileage before you request a single quote. Here is a practical method:

- Calculate your current annual mileage. Check your MOT certificates or service records. They show the odometer reading at each visit.

- Add a 10% buffer. Life changes. A new job, a house move, or a family commitment can add miles you did not plan for.

- Map that figure to the nearest mileage tier. Most leasing contracts offer tiers at 8,000, 10,000, 12,000, 15,000, and 20,000 miles per year.

- Price the next tier up. The cost difference between adjacent tiers is often £10–£20 per month. Compare that to the excess mileage rate. Upgrading is frequently cheaper.

Underestimating mileage leads to expensive penalties; overestimating inflates your monthly payment unnecessarily. Neither outcome serves you. The Lease World guide on choosing the right mileage walks through this calculation in detail if you want a step-by-step reference.

Mileage also links directly to residual value. A car returned with higher mileage than contracted is worth less to the finance company. That is why guaranteed residual values tie mileage to end-of-term charges, influencing the overall risk of the deal. Getting mileage right protects you at both ends of the contract.

What deal structures and value metrics help you compare fairly?

Not all lease deals are built the same way. Understanding the structure behind a quote stops you from comparing figures that are not actually comparable.

PCH vs PCP: the key structural difference

Personal Contract Hire is a pure rental. You make payments, use the car, and return it. There is no option to buy and no balloon payment. Personal Contract Purchase (PCP) includes a Guaranteed Minimum Future Value (GMFV), which is a large final payment you can make if you want to keep the car. The GMFV affects monthly payments because the finance company is only funding the depreciation, not the full vehicle value. Lease World's page on PCP explained covers this distinction clearly if you are weighing both options.

Using the lease value ratio to rank deals

The Lease Value Ratio (LVR) is a practical tool for comparing auto lease deals across different vehicles and payment structures. It combines your monthly payment and spread upfront cost relative to the car's retail price. LVR values below 0.8% indicate excellent deals; values above 1.5% suggest the deal is poor value. This metric is particularly useful when you are comparing a premium car on a generous deal against a budget car on a tight one.

| Metric | What it tells you | Why it matters |

|---|---|---|

| Monthly payment | Your recurring cash commitment | Easy to compare but incomplete without upfront cost |

| Total contract cost | Full cash outlay over the term | The most accurate single comparison figure |

| Lease Value Ratio | Monthly cost relative to car's retail price | Reveals whether the deal is genuinely competitive |

| Excess mileage rate | Cost per mile over the allowance | Quantifies the financial risk of underestimating usage |

Pro Tip: A cheap monthly payment on a car with a high retail price can still represent poor value. Always calculate the LVR before deciding a deal is the best car lease deal you have seen.

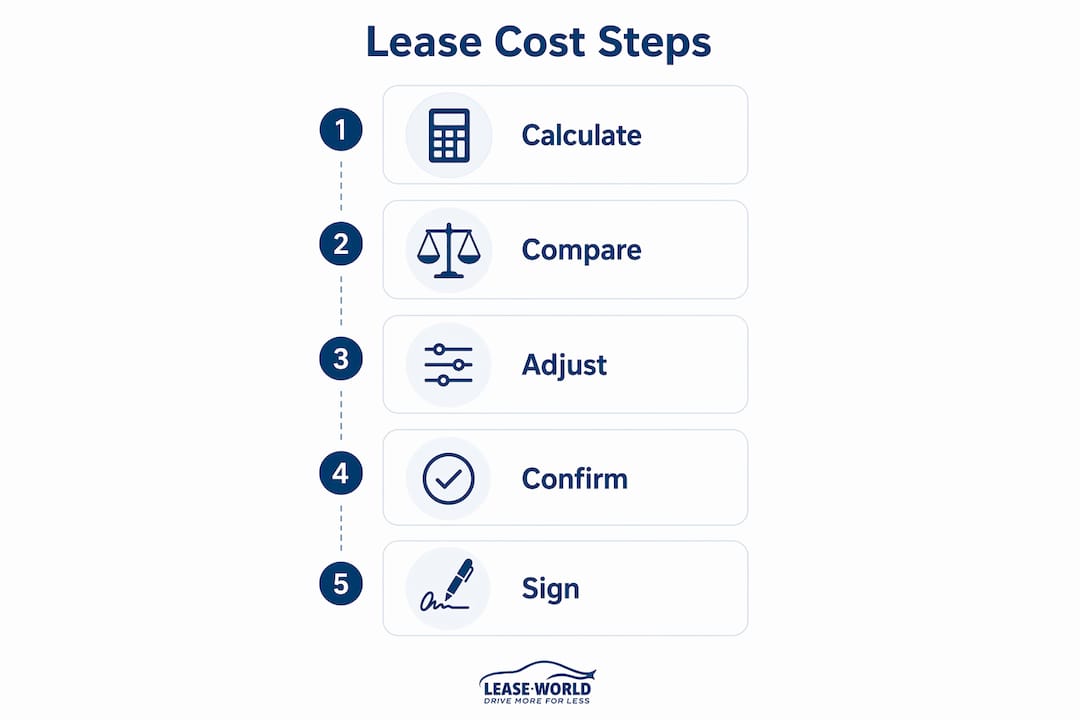

How to compare and select the best car lease deal in the UK

A structured process removes emotion from the decision and surfaces the deal that genuinely fits your needs.

- Define your mileage and term requirements first. Before you look at a single price, know your annual mileage (with buffer) and your preferred contract length. These two variables shape every quote you receive.

- Gather full deal details for each option. Collect the initial rental, monthly payment, mileage allowance, contract length, and any included maintenance. Incomplete data makes comparison impossible.

- Calculate the true monthly cost. Divide the initial rental by the number of contract months and add it to the monthly payment. This gives you a single comparable figure for every deal.

- Calculate the total contract cost. Multiply your true monthly cost by the number of months. This is your total cash commitment, and it is the fairest comparison point across the best car leasing deals UK providers offer.

- Apply the Lease Value Ratio. Divide the true monthly cost by the car's list price and express it as a percentage. Use this to rank deals by value, not just price.

- Check FCA compliance in the deal presentation. If the advertisement does not show the initial rental, term, and mileage alongside the monthly price, the provider may not be meeting its FCA transparency obligations.

- Review maintenance and end-of-lease conditions. Full maintenance packages add monthly cost but eliminate unpredictable servicing bills. Read the fair wear and tear guidelines carefully. Damage charges at return can be significant.

Watch out for these common pitfalls when looking for good car lease deals:

- Ignoring the upfront cost when comparing monthly prices

- Underestimating annual mileage and accepting a low-mileage tier to reduce monthly cost

- Missing small print on excess mileage rates, which vary widely between funders

- Assuming no deposit deals are always cheaper. Zero upfront offers are usually balanced by higher monthly rentals or longer terms

- Overlooking the difference between PCH and PCP when comparing cheap car lease deals from different brokers

Key takeaways

Comparing car lease deals requires evaluating total contract cost, mileage risk, and deal structure together, not monthly payment alone.

| Point | Details |

|---|---|

| Total cost is the benchmark | Add the spread upfront payment to monthly rentals to get a true comparable figure. |

| Mileage accuracy prevents penalties | Excess charges of 3p–15p per mile accumulate quickly; always add a 10% buffer to your estimate. |

| Deal structure changes the numbers | PCH and PCP are not directly comparable; understand the GMFV before contrasting monthly payments. |

| Lease Value Ratio ranks deals fairly | An LVR below 0.8% signals an excellent deal regardless of the car's price bracket. |

| FCA compliance signals transparency | Deals that omit initial rental, term, or mileage in their advertising may be hiding the true cost. |

What i have learned from years of watching people get lease deals wrong

The biggest mistake I see repeatedly is treating the monthly payment as the deal. Someone finds a £199 per month offer, gets excited, and signs without checking the nine-month initial rental buried in the small print. That is £1,791 upfront on a £199 deal. The true monthly cost is closer to £249 once you spread it properly.

Mileage planning deserves more attention than most people give it. I have seen drivers return cars with 8,000 miles of excess on a three-year contract. At 10p per mile, that is £800 they did not budget for. The upgrade to the next mileage tier would have cost them £15 per month, or £540 over the term. The maths was always in their favour.

My honest advice: use the Lease Value Ratio as your primary ranking tool when comparing the best car leasing deals UK brokers advertise. It cuts through the noise of different upfront structures and car price points. A deal on a £45,000 BMW with an LVR of 0.75% can be better value than a deal on a £22,000 hatchback at 1.2%. The monthly price tells you nothing useful without that context.

Work with brokers who display full cost information upfront. The FCA rules exist for good reason, and providers who comply with them are the ones worth trusting with your money.

— Jason

Find the best car lease deals UK with lease world

Lease World makes it straightforward to move from research to a real quote. The team displays full deal details, including initial rental, mileage terms, and total contract cost, so you can compare options without chasing missing figures.

Whether you are after personal car leasing or want to explore the full range of UK leasing guides before committing, Lease World's team is available to walk you through your options. There are no hidden fees, no pressure, and complimentary UK delivery on eligible vehicles. Start your search today and get a tailored quote built around your actual mileage and budget.

FAQ

What does it mean to compare car lease deals?

Comparing car lease deals means evaluating total contract cost, including upfront payment, monthly rentals, mileage allowance, and contract length, not just the advertised monthly price.

How do i calculate the true cost of a lease deal?

Divide the initial rental by the number of contract months, add it to the monthly payment, then multiply by the total term. This gives you the full cash commitment for any deal.

What are typical excess mileage charges in the UK?

Excess mileage charges range from 3p to 15p per mile depending on the funder and vehicle. A 2,000-mile annual excess over three years can cost hundreds of pounds at lease return.

What is the lease value ratio and how do i use it?

The Lease Value Ratio divides your true monthly cost by the car's retail price. Values below 0.8% indicate an excellent deal; values above 1.5% suggest you should keep looking.

Is a no deposit car lease deal always cheaper?

No. No deposit deals typically carry higher monthly payments or longer terms to compensate. Always calculate the total contract cost to confirm which structure is genuinely cheaper for your situation.