TL;DR:

- Car leasing is a fixed-term agreement allowing use of a vehicle without ownership, involving upfront payments and fixed monthly fees. Success depends on careful planning of credit, budget, mileage, and contract length, with proper management throughout the lease. At lease end, inspection, documentation, and understanding fair wear standards help avoid costly charges and facilitate smooth vehicle return.

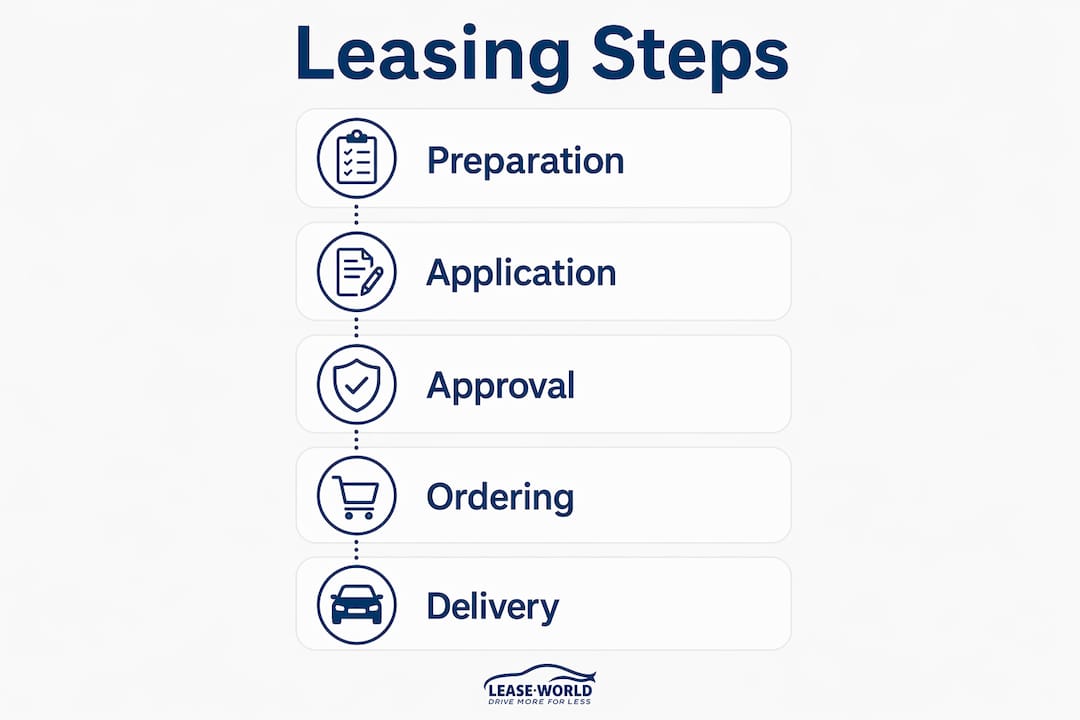

Car leasing is a fixed-term contract where you pay to use a vehicle without ever owning it, covering depreciation through an initial payment and fixed monthly instalments before returning the car at the end of the term. The car leasing process step by step moves through six distinct stages: preparation, application, approval, ordering, active management, and lease return. Understanding each stage before you sign prevents costly surprises and puts you in control of one of the most significant financial commitments many UK drivers make. This guide covers every stage in plain terms, including salary sacrifice nuances for electric vehicles, so you can approach any leasing agreement with confidence.

What do you need to decide before leasing a car?

Preparation is the stage most first-time lessees skip, and it is where the majority of costly mistakes originate. Before you contact any leasing provider, three decisions shape everything that follows: your budget, your mileage, and your contract length.

Credit score is the first practical hurdle. Leasing companies run a hard credit check during the application, so knowing your position beforehand saves wasted applications. Check your file through Experian, Equifax, or TransUnion before you start. A score below the lender's threshold does not automatically disqualify you, but it may require a larger initial payment or a guarantor.

Budget planning goes beyond the monthly payment. Factor in insurance, fuel or charging costs, and any optional maintenance package. The monthly lease cost is primarily a function of vehicle depreciation, adjusted by your chosen contract length and mileage allowance. Monthly leasing costs stay lower when your contract terms reflect your actual driving habits rather than an optimistic estimate.

Here is what to pin down before you speak to a broker:

- Contract length. Most personal leases run for 24, 36, or 48 months. Salary sacrifice EV leases most commonly run for 36 months, balancing cost and flexibility. Longer contracts reduce monthly payments but lock you in for longer.

- Annual mileage. Underestimating mileage is one of the most common and avoidable errors. Use your actual annual average, not a hopeful lower figure. Lease World's guide on choosing the right mileage walks through how to calculate this accurately.

- Vehicle type. Match the car to your genuine needs. A large SUV on a 10,000-mile annual allowance costs significantly more per month than a compact hatchback.

- Leasing type. Personal Contract Hire (PCH) is the standard route for individuals. If your employer offers it, a salary sacrifice scheme for an electric vehicle delivers tax and National Insurance savings by deducting the lease cost from your gross salary before tax is applied.

Pro Tip: If you are considering a salary sacrifice scheme, confirm with your employer's HR team whether the scheme allows mid-contract changes. Salary sacrifice contracts are typically far less flexible than personal leases, and changing vehicles or contract length mid-term can trigger financial penalties.

How do you complete the application and get finance approved?

Once your decisions are made, the formal leasing process begins with the application. Most UK leasing brokers, including Lease World, allow you to submit an application entirely online. The process is straightforward, but knowing what to expect at each step prevents delays.

- Submit your initial application. You provide personal details, employment status, residential history, and income information. This takes around 10 to 15 minutes online.

- Affordability assessment. The finance provider reviews your income against the proposed monthly payment. This is separate from the credit check and focuses on whether the commitment is sustainable relative to your outgoings.

- Credit check. A hard search is run against your credit file. Credit checks impact acceptance and the interest rate embedded in your monthly payment. Multiple applications in a short period can lower your score, so avoid applying to several providers simultaneously.

- Document submission. Once provisionally approved, you will typically need to provide proof of identity (passport or driving licence), proof of address (utility bill or bank statement dated within three months), and proof of income (recent payslips or a P60).

- Finance approval confirmation. Approval can arrive within hours for straightforward applications. More complex cases, such as self-employed applicants or those with thin credit histories, may take two to three working days.

For salary sacrifice applicants, the process differs slightly. Your employer's HR or fleet team initiates the order on your behalf through their chosen scheme provider. You still undergo a credit check in most cases, but the employer's payroll team handles the deduction mechanics rather than you arranging direct debit payments independently. Review the eligibility criteria for both routes before committing to either.

What happens from vehicle ordering through to delivery?

Finance approval triggers the ordering stage, and this is where patience becomes a practical requirement. The gap between approval and having a car on your driveway is often longer than new lessees expect.

- Confirm your specification. Once approved, you lock in the exact vehicle: make, model, trim level, colour, and any factory options. Changes after this point can restart the order or incur charges, so be certain before confirming.

- Manufacturer lead times. New car deliveries typically take 4 to 12 weeks, depending on model popularity and factory schedules. High-demand electric vehicles can sit at the longer end of that range. Pre-registered or stock vehicles are available far sooner, sometimes within days.

- Insurance. You must have fully comprehensive insurance in place before the vehicle is delivered. The leasing company owns the car throughout the contract, and most require comprehensive cover as a condition of the agreement. Arrange this before your confirmed delivery date.

- Delivery logistics. Lease World offers complimentary UK delivery on eligible vehicles, meaning the car arrives at your home or workplace without additional cost. On delivery day, inspect the vehicle thoroughly against the delivery condition report before signing acceptance.

- Salary sacrifice activation. For salary sacrifice schemes, payroll deduction activates from the delivery date. Confirm with your employer's payroll team that the start date is correctly recorded to avoid billing discrepancies.

Pro Tip: Photograph every panel, the interior, and all four tyres on delivery day. Date-stamp the images and store them securely. This documentation is invaluable if any dispute arises at the end of the lease about pre-existing marks.

How do you manage your lease during the contract period?

The active lease period is largely straightforward, but a few obligations require consistent attention to avoid charges at the end.

- Servicing. Your lease agreement specifies servicing intervals, typically aligned with the manufacturer's schedule. Use an approved garage or franchised dealer. Many lease packages include a maintenance option that covers routine servicing costs, removing the risk of unexpected bills.

- Mileage tracking. Check your odometer every three to six months against your contracted annual allowance. If you are consistently over, contact your provider to discuss adjusting the allowance before the contract ends. Excess mileage charges at return are calculated per mile and add up quickly.

- Tyres. Tyres must be replaced with the correct specification when worn. Using non-standard tyres can constitute a breach of the lease terms and result in charges at return.

- Insurance claims. Report any accident or damage to your insurer promptly. Unrepaired damage at lease return is assessed against fair wear and tear standards, which allow for minor surface marks but not dents, deep scratches, or structural damage.

For electric vehicles, fair wear and tear assessments include the battery, charging port, and any onboard software condition. Keep charging cables in good order and retain all documentation relating to software updates or battery health checks. EV-specific return criteria are more detailed than those for petrol or diesel vehicles.

What should you expect at the end of a car lease?

The lease end stage catches many drivers off guard, particularly first-time lessees who have not read the return conditions carefully. Preparation in the final two months of the contract makes a significant difference to the final bill.

End-of-lease inspections can result in unexpected charges from exceeding mileage or non-compliant wear and tear. The British Vehicle Rental and Leasing Association (BVRLA) publishes fair wear and tear guidelines that most UK leasing companies follow. Familiarise yourself with these standards before your vehicle is collected.

| Scenario | What to expect |

|---|---|

| Within mileage, good condition | No additional charges; straightforward return |

| Excess mileage | Charged per mile above the contracted allowance, as agreed in your contract |

| Fair wear and tear | Minor scuffs, light stone chips, and small interior marks are accepted without charge |

| Damage beyond fair wear | Charged at repair cost; repairing before return is often cheaper than the leasing company's rate |

| Service history incomplete | Can result in charges; retain all service records and receipts throughout the contract |

At the end of the term, you have three practical options. You can return the vehicle and walk away, which is the default. You can extend the lease on a rolling monthly or fixed-term basis if the provider offers it. In some cases, particularly with salary sacrifice schemes, you may have the option to purchase the vehicle at an agreed residual value, though this is not standard across all contracts.

Review Lease World's dedicated page on what happens at lease end for a full breakdown of the return process and your responsibilities.

Key takeaways

Leasing a car in the UK requires upfront planning on mileage, contract length, and credit health, with each stage from application to return following a defined sequence that rewards preparation.

| Point | Details |

|---|---|

| Preparation determines cost | Setting realistic mileage and contract length upfront keeps monthly payments predictable and avoids end-of-lease penalties. |

| Credit checks are unavoidable | A hard credit search runs at application; check your file with Experian or Equifax before applying to avoid surprises. |

| Delivery takes time | New vehicles typically arrive in 4 to 12 weeks; arrange insurance before the confirmed delivery date. |

| Active management prevents charges | Track mileage every few months and service the vehicle on schedule to stay within contract terms. |

| Lease end needs early preparation | Inspect and document the vehicle's condition at least two months before return to address any chargeable damage in advance. |

What I have learned from watching people navigate their first lease

Most people who struggle with leasing do not struggle because the process is complicated. They struggle because they made one or two decisions in the first ten minutes without enough information, and those decisions echoed through the entire contract.

The mileage question is the clearest example. I have seen drivers set 8,000 miles per year because it lowered their monthly payment, then rack up 12,000 miles in year one and face a penalty bill at return that wiped out every penny they had saved. The honest answer to "how many miles do you drive?" is almost always higher than the figure people initially quote.

Salary sacrifice leasing is genuinely excellent value for the right person, but it is not flexible. Mid-contract changes are restricted in ways that personal leasing is not, and I have seen people locked into a vehicle that no longer suited their circumstances because their employer's scheme had no exit mechanism. If your life or job situation is likely to change in the next three years, factor that into whether salary sacrifice is the right route.

The other thing I would tell any first-time lessee: read the fair wear and tear guide before you sign, not six weeks before return. Knowing what is and is not acceptable from day one changes how you treat the car throughout the contract. It is not about being precious with it. It is about not being surprised by a bill for something you could have fixed for £40 at a bodywork shop.

Lease World's car leasing guide is a good starting point if you want to compare contract types and understand the full range of options before committing.

— Jason

How Lease World makes the leasing process straightforward

Lease World is a family-run UK leasing provider built around transparent pricing, no hidden fees, and genuine support at every stage of the process.

Whether you are leasing your first car or switching from ownership, Lease World offers personal car leasing deals with fixed monthly payments, no-deposit options on selected vehicles, and complimentary UK delivery. The team provides tailored guidance on mileage selection, contract length, and lease terms so you choose a deal that fits your actual life rather than a generic package. Request a personalised leasing quote online in minutes and get expert support from enquiry through to delivery.

FAQ

What is car leasing and how does it differ from buying?

Car leasing is a fixed-term contract where you pay to use a vehicle without owning it, covering depreciation through monthly instalments before returning the car at the end of the term. Unlike buying, you never build equity in the vehicle, but your monthly costs are typically lower and you avoid the risk of depreciation.

How long does the car leasing process take from application to delivery?

The application and approval stage typically takes one to three working days. Once approved and the vehicle is ordered, delivery takes 4 to 12 weeks for new cars, depending on the model and manufacturer lead times.

What credit score do you need to lease a car in the UK?

There is no single universal threshold, but most finance providers require a fair to good credit score. Checking your file with Experian or Equifax before applying gives you a clear picture and helps you avoid unnecessary hard searches.

What happens if you exceed your mileage allowance on a lease?

Excess mileage is charged per mile above the contracted allowance at a rate agreed in your contract. Monitoring your odometer regularly and contacting your provider to adjust the allowance mid-contract is far cheaper than paying excess charges at return.

Can you end a car lease early?

Early termination is possible but usually carries a financial penalty, often calculated as a percentage of the remaining payments. Salary sacrifice leases are particularly restrictive in this regard, making upfront planning on contract length especially important.