TL;DR:

- Your lease monthly payment depends on residual value, capitalized cost, and the money factor, among other variables. Negotiating the vehicle price and requesting the buy rate on the money factor are the most effective ways to reduce costs. Choosing vehicles with higher residual values and minimum fees can significantly lower your monthly lease payments.

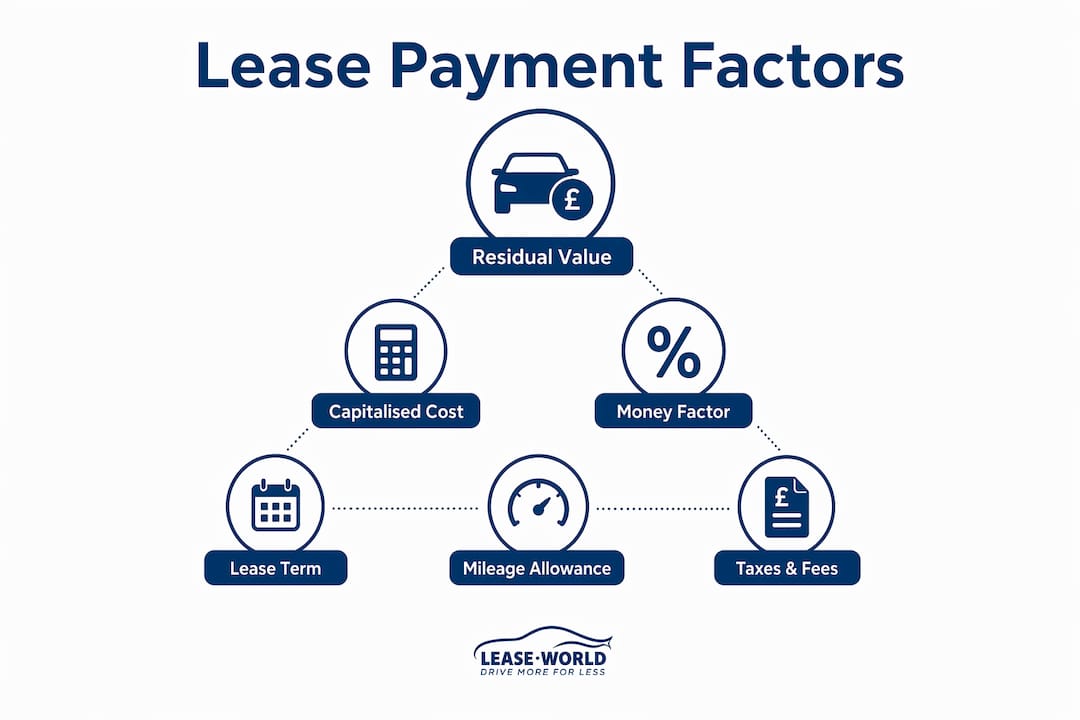

A vehicle lease monthly payment is defined by three core components: the depreciation charge, the finance charge, and applicable taxes. Understanding what affects your lease monthly payment gives you real negotiating power before you sign anything. Most people focus only on the monthly figure a dealer quotes, without realising that figure is the product of several distinct variables, each of which can be influenced. The key factors are the residual value, capitalised cost, money factor, lease term, mileage allowance, and any fees or down payment you agree to.

What affects lease monthly payment: the core formula

Monthly lease payments consist of three parts: the depreciation charge, the finance charge, and taxes. The depreciation charge is calculated by subtracting the residual value from the adjusted capitalised cost, then dividing by the number of months in the lease term. The finance charge is calculated by adding the adjusted capitalised cost and the residual value, then multiplying by the money factor. Tax is then applied on top, and the rate depends on your location.

This formula matters because it shows exactly where your money goes each month. Depreciation typically accounts for the largest share of your payment, which is why the residual value and the negotiated vehicle price have such a significant effect. The finance charge is smaller but still meaningful, and it is the part most directly tied to your credit profile and the lender's pricing decisions.

Understanding the lease payment calculation in these terms transforms a confusing monthly figure into something you can actually interrogate and, in many cases, reduce.

How does residual value affect your monthly payment?

Residual value is the estimated worth of the vehicle at the end of the lease, expressed as a percentage of the manufacturer's suggested retail price (MSRP). Higher residual values lower your monthly payment by reducing the depreciation charge, because you are only financing the portion of the vehicle's value that is expected to be used during the lease.

Most vehicles retain roughly 50% to 60% of their MSRP at lease end. A vehicle retaining 60% of its value means you only finance 40% of the purchase price through depreciation, compared to 50% for a vehicle with a lower residual. That difference can translate to a noticeably lower monthly payment, even on identically priced cars.

Residual values are set by the leasing company or manufacturer's finance arm, and they are not negotiable. However, two similar vehicles can have vastly different lease payments depending on their residual assumptions, which is why comparing models before committing is worthwhile. Residuals also vary by trim level, mileage allowance, and lease term, so the same car on a 24-month contract may carry a different residual than on a 36-month deal.

Key points about residual value:

- A higher residual percentage means lower monthly depreciation costs

- Residuals are set by the leasing company and cannot be negotiated

- Vehicles known for strong resale values, such as certain Toyota and BMW models, often produce cheaper leases for this reason

- Choosing a lower mileage allowance typically improves the residual, reducing your monthly payment

Pro Tip: Before choosing a vehicle, research its residual value percentage. A car with a 58% residual will almost always produce a lower monthly payment than a comparable car with a 48% residual, even if their sticker prices are identical.

Why does the capitalised cost change your lease payment?

The capitalised cost, often called the cap cost, is the agreed selling price of the vehicle plus any fees or extras rolled into the lease. A lower selling price reduces the capitalised cost, which lowers both the depreciation charge and the finance charge simultaneously. This is why negotiating the vehicle price before discussing lease terms is one of the most effective ways to reduce your monthly payment.

Many people make the mistake of treating a lease like a rental and skipping price negotiation entirely. The MSRP is the starting point, not the final price. Dealers are generally willing to negotiate the cap cost just as they would on a purchase, and even a modest reduction flows directly into a lower monthly figure.

Here is how cap cost reduction works in practice:

- Start with the MSRP. This is the manufacturer's listed price and your negotiation baseline.

- Negotiate the selling price down. Any reduction here directly lowers your adjusted cap cost.

- Apply any cap cost reductions. These include a down payment, trade-in value, or manufacturer incentives.

- Recalculate the adjusted cap cost. This is the figure used in both the depreciation and finance charge formulas.

- Observe the compounded saving. Because cap cost reduction influences both depreciation and finance charges, the saving is greater than it first appears.

Pro Tip: Treat the vehicle price negotiation as a completely separate conversation from the lease structure. Agree on the lowest possible selling price first, then discuss lease terms. Mixing the two allows dealers to obscure where savings are actually coming from.

What is the money factor and how does it affect your payment?

The money factor is the lease equivalent of an interest rate, expressed as a small decimal such as 0.00125. Multiplying the money factor by 2,400 gives you the approximate annual percentage rate (APR), so a money factor of 0.00125 equates to roughly 3% APR. The money factor is applied to the sum of the adjusted capitalised cost and the residual value to produce the monthly finance charge.

Your credit score is the primary factor determining which money factor you qualify for. Lenders set a base rate, known as the buy rate, and dealers are often permitted to mark this up. Dealer markups on the money factor can add £1,500 to £2,500 to the total cost of a lease, yet most customers never ask whether the quoted rate is the buy rate.

| Money factor | Equivalent APR | Monthly finance charge on £25,000 adjusted cap cost + £15,000 residual |

|---|---|---|

| 0.00083 | ~2% | ~£33 |

| 0.00167 | ~4% | ~£67 |

| 0.00250 | ~6% | ~£100 |

| 0.00333 | ~8% | ~£133 |

The table above illustrates how significantly the money factor shapes the finance portion of your monthly payment. A difference of 0.00167 in money factor doubles the finance charge. Combined with a high cap cost, a marked-up money factor is one of the most costly oversights in lease negotiations.

Factors that influence the money factor you receive:

- Credit score: higher scores typically secure lower money factors

- Market interest rates: lenders adjust buy rates in line with broader rate movements

- Manufacturer promotions: some brands subsidise money factors on specific models to stimulate demand

- Dealer markup: always ask for the buy rate and confirm whether the quoted money factor includes any markup

How do lease term and mileage allowance shape your costs?

Lease term length and annual mileage allowance are two of the most practical levers available to you when structuring a lease. Lease terms typically run from 12 to 36 months, and a longer term spreads the depreciation charge over more payments, reducing the monthly amount. However, a longer term also means the finance charge accrues over more months, which can increase the total cost of the lease even as the monthly figure falls.

You can explore the trade-offs in more detail through Lease World's car lease term length guide, which covers how contract length affects both monthly payments and overall expenditure.

Mileage allowance has a direct effect on residual value. Higher mileage allowances reduce the residual because the vehicle is expected to be worth less at lease end after covering more miles. This increases the depreciation charge and raises your monthly payment. The relationship works in reverse too: choosing a lower mileage limit improves the residual and reduces your monthly cost.

Key considerations for mileage and term decisions:

- Underestimating your mileage leads to excess mileage penalties at lease end, which are typically charged per mile and can be substantial

- Overestimating mileage means paying for miles you never use through a higher monthly payment

- A 24-month lease generally carries a higher monthly payment than a 36-month lease on the same vehicle, but the total finance charge is usually lower

- If you can increase mileage on a car lease mid-contract, doing so early is almost always cheaper than paying excess mileage charges at the end

What role do taxes, fees, and down payments play?

Taxes and fees are the components of a lease payment breakdown that most people underestimate. Lease fees including acquisition, disposition, and registration costs typically add several hundred pounds to the total lease cost. Acquisition fees alone can range from £500 to £900, and while some are non-negotiable, others can be waived or reduced, particularly for repeat customers.

Here is a structured view of the main additional costs to review before signing:

- Acquisition fee. Charged by the leasing company to arrange the finance. Often rolled into the cap cost, which means you pay interest on it throughout the lease.

- Disposition fee. Charged at lease end if you do not purchase the vehicle or re-lease with the same company. Sometimes waivable.

- Registration and documentation fees. Vary by region and are generally non-negotiable.

- Sales tax. Applied either on the monthly payment or as a lump sum upfront, depending on jurisdiction.

Down payments, or initial rental payments in UK leasing terminology, reduce the adjusted capitalised cost and therefore lower your monthly payment. However, a down payment is typically non-refundable. If the vehicle is written off or stolen, your insurer reimburses the leasing company, not you. You lose the upfront sum entirely.

Pro Tip: Keep your initial rental payment as low as practically possible. The monthly saving from a large upfront payment rarely justifies the financial risk of losing it in a total loss event. Spread the cost through the monthly payment instead.

For a full breakdown of what is and is not included in a standard agreement, Lease World's guide on what is included in a car lease covers the detail clearly.

Key takeaways

Monthly lease payments are determined by six variables: residual value, capitalised cost, money factor, lease term, mileage allowance, and fees. Negotiating the cap cost and asking for the buy rate on the money factor are the two highest-impact actions available to any lessee.

| Point | Details |

|---|---|

| Residual value drives depreciation | A higher residual percentage directly reduces your monthly depreciation charge. |

| Cap cost is negotiable | Reducing the selling price lowers both the depreciation and finance charge simultaneously. |

| Money factor markups are common | Always ask for the buy rate; dealer markups can add over £1,500 to total lease cost. |

| Mileage affects residual | Choosing a lower mileage allowance improves the residual and reduces monthly payments. |

| Down payments carry risk | Upfront payments are non-refundable and lost entirely in a total loss event. |

The factor most people ignore when leasing

Most people who come to Lease World having already visited a dealership have done one thing well: they negotiated the vehicle price. What they almost never did was ask about the money factor. In my experience, this is the single most overlooked variable in the entire lease payment calculation, and it is the one dealers have the most discretion over.

The money factor is the lease's disguised interest rate, and comparing it alongside residual and cap cost gives you the clearest picture of what a lease actually costs. A dealer can show you a lower monthly payment by extending the term while quietly marking up the money factor. The monthly figure looks attractive, but the total cost over the contract is higher than it needed to be.

My practical advice is this: before you agree to any lease, convert the money factor to an APR by multiplying by 2,400. If that APR seems high relative to current market rates, ask the dealer to confirm whether the quoted money factor is the buy rate. You are entitled to that information, and a reputable leasing company will give it to you without hesitation.

The other pitfall I see regularly is people choosing vehicles without checking residual values first. Two cars at the same price can produce monthly payments that differ by £50 or more, purely because of residual assumptions. Choosing a vehicle with a strong residual is one of the easiest ways to lower your payment without negotiating anything at all.

— Jason

Find your best lease deal with Lease World

Lease World makes the leasing process straightforward by being transparent about every factor that shapes your monthly payment. Whether you are looking at personal car leasing, window van lease deals, or electric vehicles, Lease World provides fixed monthly payments with no hidden fees and no deposit options on eligible vehicles. The team compares contracts across a wide range of vehicles to find the arrangement that fits your budget and driving habits. If you want to go deeper on any of the factors covered in this article, the Lease World leasing guides cover everything from residual values to contract types in plain language. Ready to see what your monthly payment could look like? Request a personalised quote and get a clear, tailored figure with no obligation.

FAQ

What is the biggest factor in a lease monthly payment?

Depreciation is the largest component of most lease payments, determined by the difference between the capitalised cost and the residual value divided by the lease term. Choosing a vehicle with a high residual value is the most effective way to reduce this portion.

How does my credit score affect my lease payment?

Your credit score influences the money factor you are offered, which determines the finance charge portion of your monthly payment. A stronger credit profile typically secures a lower money factor and therefore a lower monthly cost.

Can I negotiate a lower monthly lease payment?

Yes. Negotiating the vehicle's selling price (cap cost) and asking for the buy rate on the money factor are the two most effective negotiation points. Selecting a lower mileage allowance and a longer lease term can also reduce the monthly figure.

Is a large down payment on a lease a good idea?

A large down payment reduces your monthly payment but is non-refundable. If the vehicle is written off or stolen, you lose the upfront sum entirely, making a smaller initial payment the lower-risk choice for most lessees.

What fees should I expect on top of the monthly lease payment?

Common lease fees include an acquisition fee (typically £500 to £900), a disposition fee at lease end, registration costs, and sales tax. Some fees are negotiable, particularly for returning customers or as part of a promotional offer.