TL;DR:

- The leasing company retains legal ownership of a leased car throughout the contract, while the lessee is only the registered keeper responsible for insurance and maintenance. The V5C document shows the keeper's details but does not prove ownership, which remains with the finance provider. At lease end, the vehicle is returned unless a purchase option is exercised, transferring ownership only upon full payment.

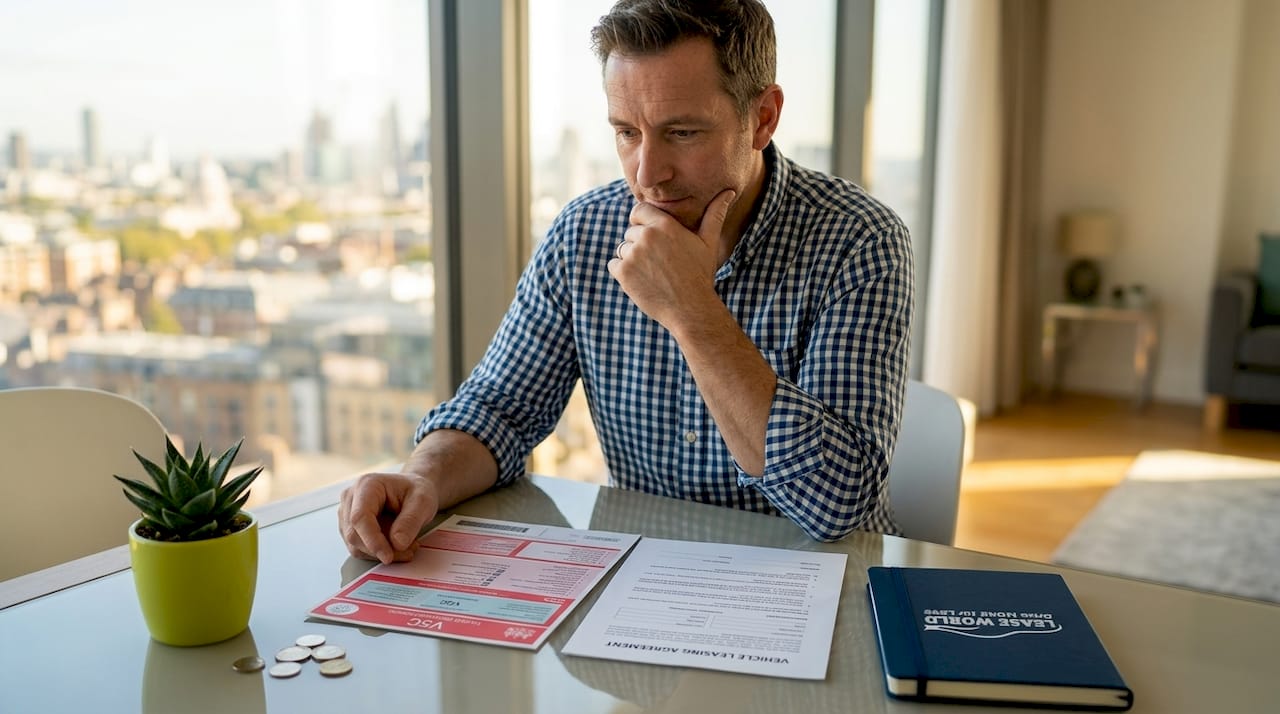

The leasing company or finance provider owns a leased car, not the individual driving it. This is the single most misunderstood fact in UK vehicle leasing, and it has real consequences for insurance, accident liability, and what happens when your contract ends. You are the registered keeper, a legal status defined by the DVLA that carries responsibility for tax and insurance but confers no ownership rights whatsoever. Understanding this distinction before you sign protects you from costly mistakes.

Who owns a leased car: legal title vs registered keeper

Legal ownership of a leased vehicle sits with the finance or leasing company throughout the entire contract term. The V5C logbook records the registered keeper, not the legal owner, which is why your name appears on the document even though you have no title to the vehicle. The DVLA issues the V5C purely to track who is responsible for taxing and insuring the car, not to confirm who holds the asset.

Many lessees assume that holding the V5C means they legally own the car. This is one of the most common misconceptions in UK motoring and regularly causes confusion during accidents and insurance claims. The document is an administrative record, not a title deed.

Here is what each status actually means in practice:

- Legal owner: The leasing or finance company. They hold the title, can repossess the vehicle if payments lapse, and retain the asset on their balance sheet.

- Registered keeper: You, the lessee. The registered keeper is responsible for Vehicle Excise Duty (road tax), insurance, and ensuring the car is roadworthy.

- Driver: Could be you or any named driver on your insurance policy, subject to the leasing company's approval.

The separation matters because it defines who can sell the car, who bears financial risk if it is written off, and who must be notified in the event of an accident.

Pro Tip: Never assume the V5C grants ownership. If you are ever in doubt about who holds legal title to your leased vehicle, contact your leasing company directly and ask for written confirmation.

Who is responsible for a leased car during the contract?

Responsibility and ownership are two different things in a lease agreement, and the lessee carries most of the day-to-day obligations. The finance company retains ownership and sets the rules, but you are accountable for keeping the vehicle in good order throughout the term.

Your core responsibilities as a lessee typically include:

- Arranging insurance. Lease car insurance must meet the standards set by your leasing company, which are usually higher than the legal minimum. Comprehensive cover is almost always required.

- Maintaining the vehicle. Routine servicing, tyre replacements, and general upkeep fall to you. Returning a car in poor condition results in excess wear-and-tear charges.

- Staying within the agreed mileage. Exceeding your contracted annual mileage triggers per-mile penalty charges at the end of the term.

- Reporting accidents promptly. You must notify both your insurer and the leasing company after any collision, regardless of fault. The leasing company sets rules on approved repairers, and using an unapproved garage can breach your contract.

- Complying with usage terms. Most leases prohibit subletting the vehicle or using it for hire and reward without prior written consent.

The leasing company's responsibilities are narrower. They supply the vehicle, maintain the finance arrangement, and handle the asset at the end of the term. They do not cover your day-to-day running costs.

Pro Tip: Read the fair wear-and-tear guidelines your leasing company provides at the start of the contract. The British Vehicle Rental and Leasing Association (BVRLA) publishes a widely used standard that most UK leasing firms follow.

How ownership affects what happens at the end of the lease

Because the leasing company holds legal title throughout, you do not accumulate equity in the vehicle the way you would with a hire purchase or outright purchase agreement. At the end of a standard Personal Contract Hire (PCH) or Business Contract Hire (BCH) lease, you simply return the car. The asset appreciation or depreciation belongs entirely to the finance company.

The table below compares the most common end-of-lease outcomes and how ownership factors into each:

| End-of-lease option | Who holds ownership | Does the lessee gain equity? |

|---|---|---|

| Return the vehicle | Finance company retains title | No |

| Extend the lease | Finance company retains title | No |

| Purchase the vehicle (if permitted) | Transfers to lessee on payment | Yes, from point of purchase |

| Voluntary termination | Finance company retains title | No |

Legal ownership transfers only if a purchase option is exercised and the agreed sum is paid in full. Standard contract hire agreements do not include a purchase option at all, which is the fundamental difference between leasing and hire purchase. If building equity in a vehicle matters to you, leasing is the wrong product.

The end-of-lease process is also where ownership confusion causes the most financial pain. Lessees who believe they have some claim to the vehicle sometimes resist returning it or dispute damage charges. The contract is unambiguous: the car belongs to the finance company, and the lessee's obligation is to return it in the agreed condition.

Common questions about leased car ownership answered

Can I sell a leased car?

No. Because legal title belongs to the finance company, you have no right to sell the vehicle. Attempting to do so would constitute fraud. If you need to exit the contract early, contact your leasing company to discuss early termination options, which will typically involve a settlement fee.

Who insures a leased car?

The lessee arranges and pays for insurance, but the leasing company dictates the minimum level of cover required. Comprehensive insurance is the standard requirement across the UK leasing market. The policy must also note the finance company's interest in the vehicle.

What happens if the car is written off?

Your insurer pays the market value of the vehicle at the time of the write-off. If that figure is lower than the outstanding finance balance, you face a shortfall. Gap insurance covers this difference and is strongly recommended for leased vehicles, particularly in the early months of a contract when depreciation is steepest.

Does the lessee get any equity?

No. Under a standard contract hire arrangement, the lessee receives no equity, no residual value, and no ownership rights. The finance company absorbs any change in the vehicle's market value. This is the trade-off for fixed monthly payments and no large upfront capital outlay.

What if the car is defective?

Lessees retain consumer protections under UK warranty legislation and, where applicable, lemon law equivalents. Lemon law provisions provide recourse for persistently defective vehicles, requiring communication between the lessee and the leasing company to resolve the issue. Not owning the car does not strip you of your consumer rights.

How to verify ownership and responsibility for a leased vehicle

Checking the ownership status of a leased vehicle is straightforward if you know where to look. The V5C is your starting point, but it only tells part of the story. Verifying outstanding finance and confirming the leasing company's identity protects you from entering an agreement with complications attached.

The table below outlines the key checks and what each one reveals:

| Verification method | What it confirms | Limitation |

|---|---|---|

| V5C logbook | Registered keeper identity | Does not confirm legal ownership |

| HPI or vehicle history check | Outstanding finance, theft record, write-off history | Requires payment; snapshot in time |

| Contact leasing company directly | Legal owner identity, contract terms | Requires account access or written request |

| Thatcham-approved tracker records | Vehicle security compliance, ownership definitions | Specific to security-related documentation |

An HPI check is the most practical tool for confirming whether a vehicle has outstanding finance registered against it. If you are taking over a lease from another driver or entering a used-car lease arrangement, this check is non-negotiable. A vehicle with undisclosed finance attached to it can be repossessed by the creditor regardless of what you paid or agreed.

Signs that documentation may not reflect true ownership include a V5C name that does not match the leasing company named in your contract, a vehicle history showing a previous private owner with no record of the finance being settled, or a leasing company that cannot provide written confirmation of their legal title. Any of these warrants further investigation before you proceed.

Key takeaways

The leasing company holds legal title to a leased car throughout the contract; the lessee is the registered keeper with responsibility for insurance, maintenance, and compliance but no ownership rights.

| Point | Details |

|---|---|

| Legal owner is the finance company | The leasing firm holds title throughout; you cannot sell or claim equity in the vehicle. |

| V5C shows keeper, not owner | The DVLA document records your responsibility for tax and insurance, not legal ownership. |

| Lessee carries day-to-day responsibility | Insurance, servicing, mileage limits, and accident reporting all fall to you under the contract. |

| No equity at standard lease end | Returning the car means the finance company keeps any residual value; purchase options transfer title only on full payment. |

| Verify ownership before signing | An HPI check and direct confirmation from the leasing company protect you from undisclosed finance or ownership disputes. |

What I have learned from years of watching lessees get this wrong

The ownership question sounds simple until someone has an accident or tries to exit a contract early. I have seen lessees genuinely believe they could sell their leased car privately because their name was on the V5C. The shock when they discover the finance company can repossess the vehicle is real, and it is entirely avoidable.

The most costly mistake I see is people skipping the lease agreement details entirely and relying on a verbal summary from a broker. The contract is the only document that matters. It defines who owns the car, what you owe if you return it damaged, what happens if you exceed the mileage, and whether you have any purchase rights at all. Reading it takes thirty minutes. Ignoring it can cost thousands.

My honest view is that leasing is an excellent product for people who want a new car every two to four years without the depreciation risk. But it only works in your favour when you understand that you are renting, not buying. The moment you start treating a leased car as your own asset, you make decisions that the contract does not support.

One practical step that most lessees overlook: keep a written record of every communication with your leasing company, particularly around damage, mileage, and early termination. If a dispute arises at the end of the term, that paper trail is your only defence. The leasing company has the contract and the legal title. You need documentation to protect your position.

— Jason

Explore leasing options and guides with Lease World

Understanding who owns a leased car is the foundation of a confident leasing experience. At Lease World, we go further than just handing you a contract. Our leasing guides cover everything from insurance requirements to end-of-lease processes, written in plain English for UK drivers. If you are ready to find a deal that suits your budget and lifestyle, browse our personal car leasing options with fixed monthly payments, no hidden fees, and free UK delivery on eligible vehicles. Our team is available to answer your ownership and responsibility questions before you commit.

FAQ

Who legally owns a leased car in the UK?

The leasing company or finance provider holds legal title to a leased car throughout the contract term. The lessee is the registered keeper, responsible for tax and insurance, but has no ownership rights.

Does the V5C prove I own my leased car?

No. The V5C records the registered keeper for DVLA purposes and is not proof of legal ownership. The finance company retains title even though your name appears on the document.

Can I buy my leased car at the end of the contract?

Only if your lease agreement includes a purchase option. Standard Personal Contract Hire and Business Contract Hire agreements do not include this option; legal ownership transfers only when the agreed purchase price is paid in full.

Who is responsible for insuring a leased car?

The lessee arranges and pays for insurance, but must meet the standards set by the leasing company. Comprehensive cover is almost universally required, and the policy must note the finance company's interest in the vehicle.

What happens to equity in a leased car?

Under a standard contract hire lease, the lessee receives no equity. Any residual value in the vehicle at the end of the term belongs to the finance company. This is the core trade-off for predictable monthly payments and no capital outlay.