TL;DR:

- A personal car lease, known as Personal Contract Hire, is a fixed-term rental where you pay monthly without owning the vehicle. It offers lower payments and flexibility, but lacks early termination rights, making contract review and mileage planning crucial. Most leases last two to three years, with strict mileage caps and conditions that require careful negotiation and documentation to prevent costly penalties.

A personal car lease is the rental of a vehicle under a fixed-term contract, where you pay a set monthly amount for use of the car without ever owning it. Known formally as Personal Contract Hire (PCH), it is one of the most popular ways to drive a new car in the UK today. Monthly payments are typically lower than those on a finance agreement because you are paying for the vehicle's depreciation over the contract period, not its full value. Most PCH contracts run for two to three years, with an agreed annual mileage limit and a fixed payment schedule that makes budgeting straightforward.

What are the key terms in a personal car lease?

Understanding car lease terminology is the single most important step before signing any contract. The language used in PCH agreements can appear technical, but each term maps to a real cost or condition you will live with for the duration of the lease.

Here are the core terms you need to know:

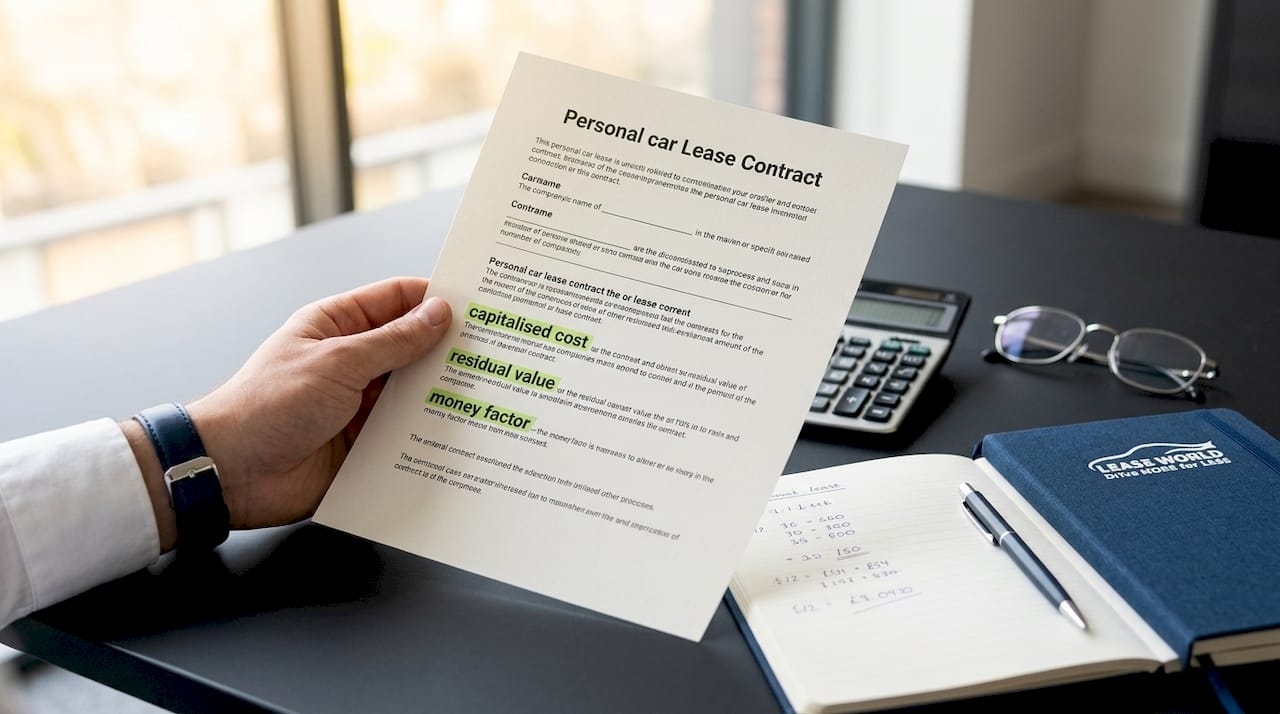

- Capitalised cost: The agreed value of the vehicle at the start of the lease. A lower capitalised cost reduces your monthly payments, so negotiating this figure down is worthwhile.

- Residual value: The predicted value of the car at the end of the contract. A higher residual value means lower monthly payments, because less depreciation is being financed.

- Money factor: The finance charge built into your lease, expressed as a small decimal. Multiply it by 2,400 to convert it to an approximate annual percentage rate.

- Mileage cap: The maximum annual mileage agreed in the contract. Mileage caps typically range between 10,000 and 15,000 miles per year in UK leases, and exceeding them triggers a per-mile penalty charge.

- Acquisition fee: A one-off administration charge levied by the finance company at the start of the lease.

- Disposition fee: A charge applied at lease end if you choose not to take out a new lease with the same provider.

- Initial rental: The upfront payment made before the contract begins, usually equivalent to three to nine monthly payments.

Leasing a car means your monthly payment is calculated on the gap between the capitalised cost and the residual value, plus the money factor applied to the combined total. That structure is why PCH payments are lower than loan repayments on the same vehicle.

Pro Tip: Ask the dealer or broker to confirm the money factor and capitalised cost in writing before you sign. Both figures are negotiable, and reducing either one directly lowers your monthly outgoing.

Insurance and routine maintenance are your responsibility throughout the lease. Some contracts include a maintenance package that covers servicing and tyres for an additional monthly fee, which can simplify budgeting considerably.

Leasing vs buying: what are the real differences?

The leasing vs buying decision comes down to priorities: lower short-term cost and flexibility versus long-term ownership and equity.

| Aspect | Personal leasing (PCH) | Buying outright or on finance |

|---|---|---|

| Monthly cost | Lower, based on depreciation only | Higher, covers full vehicle value |

| Ownership | None. Car is returned at contract end | Full ownership once paid |

| Mileage | Capped annually | Unlimited |

| Equity | No equity built | Asset value retained |

| Warranty | Usually covered throughout lease term | Expires after manufacturer period |

| Flexibility | Fixed term, early exit is costly | Can sell at any time |

| Upfront cost | Initial rental required | Deposit or full payment |

The primary financial advantages of leasing are lower monthly payments and the ability to drive a new car every two to three years. Those advantages come with a clear trade-off: you build no equity, and the car is never yours. For drivers who prioritise having the latest model, reliable warranty cover, and predictable costs, PCH is a strong fit. For those who drive high mileage or want to own an asset outright, buying makes more financial sense over the long term.

Mileage penalties deserve particular attention. Exceeding your agreed annual limit by even a few thousand miles can add hundreds of pounds to your final bill. Before agreeing a mileage cap, review your last two years of driving records and add a buffer of at least 1,000 miles per year.

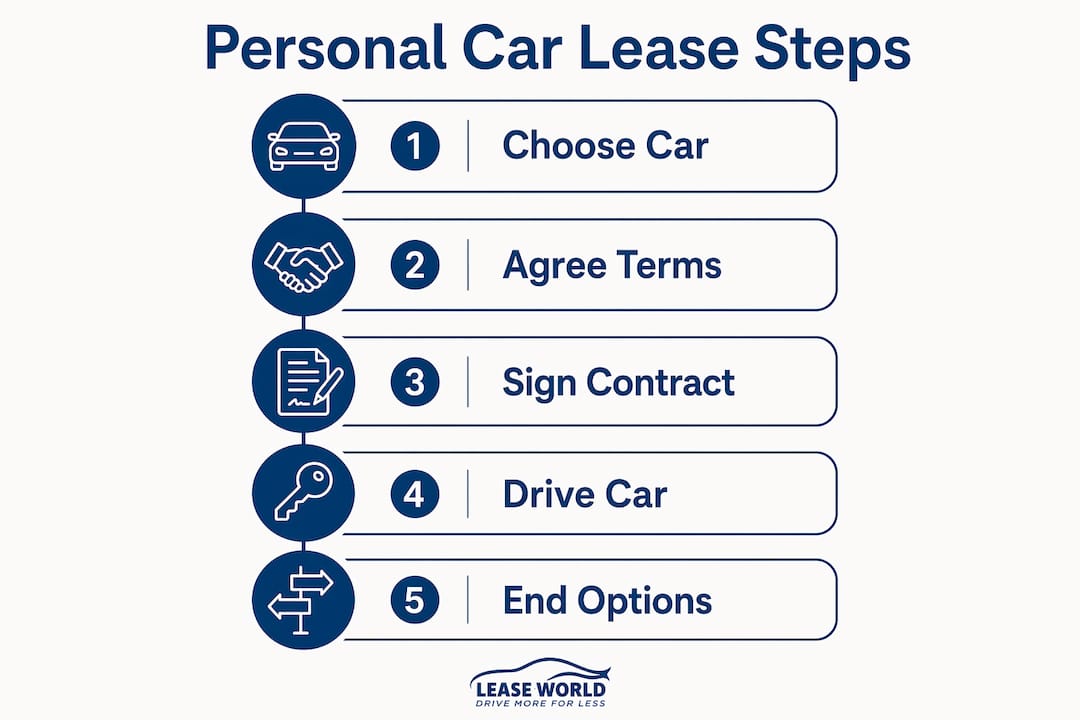

How does the personal car leasing process work in the UK?

The leasing process in the UK follows a clear sequence, and knowing each step prevents costly surprises.

- Check your credit score. Leasing companies assess your credit history before approving a PCH application. A strong score improves your chances of approval and may unlock better rates. Check your report via Experian, Equifax, or TransUnion before applying.

- Choose your vehicle and contract terms. Select the make, model, and specification you want, then agree the contract length (typically 24 or 36 months), annual mileage, and initial rental amount. A higher initial rental reduces your monthly payments.

- Review leasing eligibility requirements. You must be a UK resident, hold a valid driving licence, and meet the finance company's income and credit criteria.

- Read the contract in full. Pay close attention to the mileage limit, fair wear and tear policy, early termination clauses, and any additional fees. Do not rely on verbal summaries.

- Arrange insurance. Fully comprehensive cover is mandatory on a leased vehicle. The finance company owns the car, so they require the highest level of protection. Review your lease car insurance options before the vehicle is delivered.

- Take delivery and document the condition. Photograph the vehicle thoroughly on the day it arrives. This protects you against any disputed damage claims when you return it.

- Return the vehicle at lease end. Returning the vehicle requires it to be in good condition within the fair wear and tear guidelines set by the British Vehicle Rental and Leasing Association (BVRLA). Excess damage or mileage overrun results in additional charges.

Pro Tip: Book an independent pre-return inspection two to four weeks before your contract ends. This gives you time to address any minor damage before the official handover, potentially saving you from inflated repair charges levied by the leasing company.

At lease end, you typically have three options: return the car and walk away, start a new lease on a different vehicle, or in some cases negotiate a purchase of the existing car. Most PCH customers choose to start a fresh lease.

What happens if you need to end a personal lease early?

Early termination of a PCH contract is one of the most misunderstood areas of personal vehicle leasing, and it carries real financial risk.

PCH agreements do not include Voluntary Termination (VT) rights under the Consumer Credit Act. This is a critical distinction. VT rights allow consumers to exit regulated Hire Purchase (HP) or Personal Contract Purchase (PCP) agreements early once they have paid 50% of the total amount payable, under Section 99 of the Consumer Credit Act. Because PCH is a rental agreement rather than a regulated finance product, VT rights apply only to HP and PCP contracts, not to personal leases.

Your exit options under a PCH contract are more limited:

- Break clause: Some contracts include a break clause allowing early exit after a specified period, usually at the halfway point. This is not standard, so check your contract before signing.

- Early termination fee: Most PCH providers charge a fee of approximately 50% of remaining payments if you exit early without a break clause. On a three-year lease with 18 months remaining, that figure can be substantial.

- Lease transfer: Some providers allow you to transfer the lease to another person, though this depends on the finance company's approval and the new lessee's credit profile.

- Paying off the full remaining balance: In some cases, settling all outstanding payments is the only route to returning the vehicle early.

| Exit option | Availability | Typical cost |

|---|---|---|

| Break clause | Contract-specific | Minimal or nil if included |

| Early termination fee | Standard in most PCH contracts | Around 50% of remaining payments |

| Lease transfer | Subject to provider approval | Administration fee |

| Full settlement | Always available | All remaining monthly payments |

The practical advice here is straightforward: if there is any chance your circumstances could change during the contract period, negotiate a break clause before you sign. Once the contract is active, your options narrow considerably.

Key takeaways

A personal car lease (PCH) offers lower monthly costs and access to new vehicles, but the absence of Voluntary Termination rights and strict mileage limits make contract scrutiny non-negotiable before signing.

| Point | Details |

|---|---|

| PCH is rental, not ownership | You pay for depreciation and return the car at contract end with no equity gained. |

| VT rights do not apply to PCH | Unlike HP or PCP, you cannot use Section 99 of the Consumer Credit Act to exit early. |

| Mileage caps carry real penalties | Exceeding your agreed annual limit triggers per-mile charges; always build in a buffer. |

| Money factor is negotiable | Ask for the money factor in writing and negotiate it down to reduce your monthly cost. |

| Document condition on delivery and return | Photographs protect you from disputed damage charges at both ends of the contract. |

What I have learnt from watching people get caught out by PCH contracts

The single most common mistake I see is treating a personal car lease like a phone contract. People assume they can hand the car back whenever they like and move on. The reality is that PCH is a rental agreement with no statutory exit route, and that distinction costs people real money every year.

The early termination issue is the sharpest edge. Most drivers do not read the termination clause until they need to use it, at which point they discover that exiting costs roughly half of what they still owe. Negotiating a break clause at the outset takes five minutes and can save thousands.

Mileage restrictions are the second trap. Drivers consistently underestimate how much they drive, particularly when life changes: a new job, a house move, a growing family. I would always recommend reviewing your actual mileage from the past two years before agreeing a cap, then adding a buffer rather than trying to save a few pounds per month on a tighter limit.

On the positive side, PCH genuinely suits a large proportion of UK drivers. If you want a new car every two to three years, prefer fixed and predictable costs, and do not want the hassle of depreciation risk or selling a used car, leasing is a rational choice. Electric vehicle leasing in particular is worth exploring in 2026, as residual values on EVs remain volatile and leasing transfers that depreciation risk to the finance company rather than you.

Read the contract. Photograph the car. Negotiate the money factor. Those three habits will protect you from the vast majority of leasing disputes.

— Jason

Find your next personal lease with Lease World

Lease World offers a range of personal car leasing deals across the UK, with fixed monthly payments, no hidden fees, and complimentary delivery on eligible vehicles. As a family-run business, Lease World provides the kind of personalised support that larger brokers rarely match, including detailed contract comparisons and honest advice on terms before you commit. Whether you are leasing for the first time or switching from a previous agreement, you can explore the full range of leasing guides to build your knowledge, or request a personalised quote directly to see what is available for your budget and requirements.

FAQ

What is a personal car lease in the UK?

A personal car lease, formally known as Personal Contract Hire (PCH), is a fixed-term rental agreement where you pay monthly to use a vehicle without owning it. At the end of the contract, you return the car to the finance company.

How does a personal lease differ from PCP?

PCP (Personal Contract Purchase) is a regulated finance product that includes an option to buy the car at the end of the term and carries Voluntary Termination rights under the Consumer Credit Act. PCH is a rental agreement with no ownership option and no VT rights.

Can I end a personal car lease early?

PCH contracts do not carry Voluntary Termination rights, so early exit typically requires paying around 50% of remaining payments unless your contract includes a break clause. Always check the termination terms before signing.

What mileage limits apply to personal leases?

Most UK personal leases set annual mileage caps between 10,000 and 15,000 miles. Exceeding the agreed limit results in a per-mile excess charge applied at the end of the contract.

Do I need fully comprehensive insurance on a leased car?

Fully comprehensive insurance is mandatory on all leased vehicles in the UK. The finance company retains ownership of the car throughout the contract and requires the highest level of cover as a condition of the agreement.